The 2026 stablecoin market reality

The numbers tell a story of explosive, structural growth. According to data from Allium and Visa, the global fiat-backed stablecoin supply exceeded $273 billion in March 2026 1. This figure represents a 40x increase from the $6.8 billion recorded in March 2020. The market has moved far beyond the speculative fringes of DeFi into the bloodstream of global finance.

This scale changes the competitive calculus entirely. Native stablecoin infrastructure is no longer just a technical feature for developers to tinker with; it is a critical competitive moat. As transaction volumes scale, the underlying rails determine speed, cost, and reliability. Projects that rely on legacy bridges or inefficient wrapping mechanisms are losing ground to those with purpose-built, native settlement layers.

The shift from a niche primitive to global financial infrastructure is complete. Investors and institutions now demand infrastructure that can handle billions in daily volume without the latency or counterparty risks associated with older models. The market is rewarding those who treat stability and speed as foundational, not optional.

Settlement rails and orchestration layers

Native stablecoin infrastructure has matured into two distinct technical paths: custodial settlement APIs and non-custodial middleware. The choice between these models defines how much control a business retains over its funds and how much friction exists in cross-border payments.

Custodial settlement APIs, such as those offered by Circle or Stripe, handle the underlying blockchain interactions on behalf of the merchant. This approach simplifies integration but requires trusting a third party with the keys. Non-custodial middleware, by contrast, allows developers to own the keys and manage transactions directly. This split is the clearest structural division in the current market landscape.

The following comparison outlines the operational differences between these two infrastructure models.

| Model | Control | Compliance Burden | Settlement Speed |

|---|---|---|---|

| Custodial API | Third-party managed | Provider-led | Instant (off-chain) |

| Non-custodial Middleware | Self-managed keys | Self-managed | Variable (on-chain) |

| Hybrid Orchestrator | Shared responsibility | Automated routing | Near-instant |

For cross-border payments, native infrastructure reduces friction by bypassing traditional correspondent banking layers. When businesses use non-custodial middleware, they can route settlements through the most efficient stablecoin rails in real time. This reduces reliance on legacy payment networks and minimizes the delays associated with international wire transfers.

The market for these infrastructure providers continues to consolidate, with major players focusing on interoperability between custodial and non-custodial systems. As 2026 progresses, the ability to seamlessly switch between these models will likely become a standard feature for enterprise-grade stablecoin solutions.

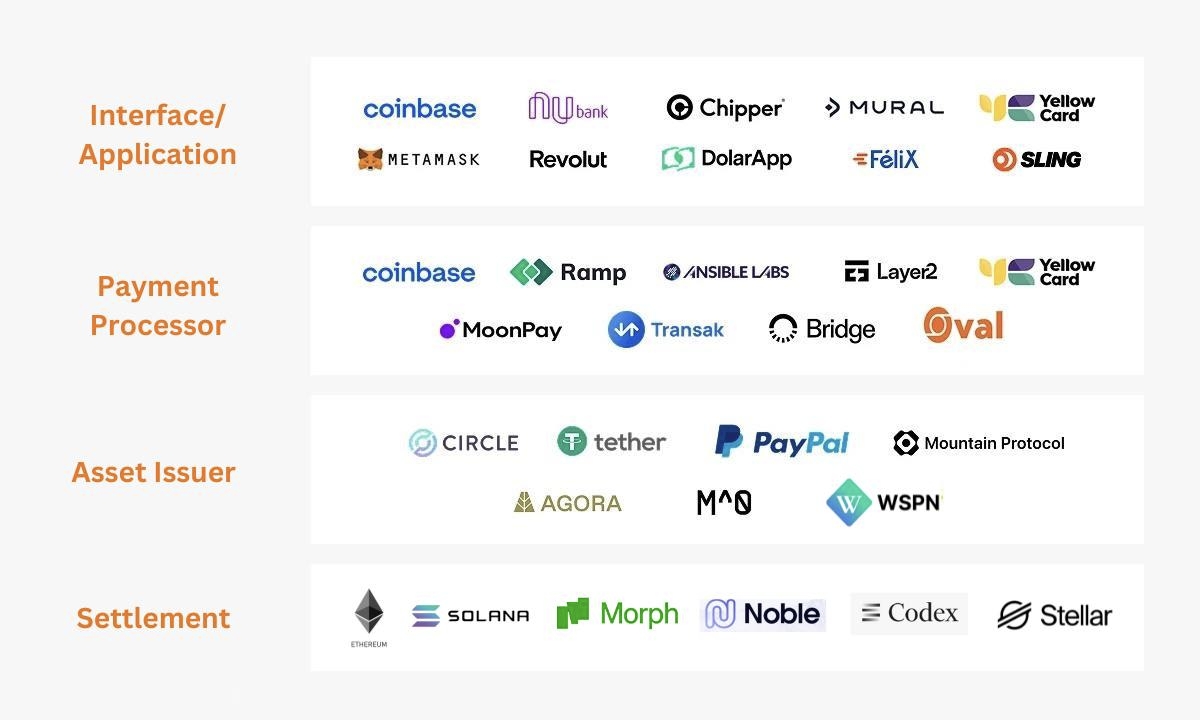

Key infrastructure providers in 2026

The native stablecoin ecosystem relies on three dominant infrastructure pillars: Bridge, Rain, and Chainlink. Each plays a distinct role in moving value across the blockchain landscape, from issuance and payments to cross-chain liquidity.

Bridge operates as an end-to-end platform for stablecoin infrastructure. It provides the APIs and tools needed to receive, store, convert, issue, and spend stablecoins. For businesses, Bridge consolidates these functions into a single platform, simplifying the complex backend of stablecoin operations. Visit Bridge to explore their developer-focused solutions.

Rain focuses specifically on enterprise payments. It powers stablecoin-enabled cards and facilitates global money movement with a scalable API. The platform prioritizes fast settlement and reliability, making it a go-to for financial institutions looking to integrate stablecoin payments into existing systems. Learn more about Rain.

Chainlink serves as the connective tissue for native stablecoins. Its oracle platform ensures accurate price data across different blockchains, while its Cross-Chain Interoperability Protocol (CCIP) unifies liquidity. This allows stablecoins to move seamlessly between networks, maintaining stability and accessibility regardless of where the user is. See Chainlink's stablecoin use cases.

USDT Market Context

Understanding the scale of the stablecoin market helps contextualize the importance of these providers. Tether (USDT) remains the largest stablecoin by market capitalization, serving as a primary benchmark for market stability and volume.

Enterprise adoption and strategy

The conversation around native stablecoin infrastructure has shifted from theoretical potential to active integration. Major financial institutions and technology providers are no longer just experimenting; they are embedding tokenized cash directly into the workflows that drive global commerce. This shift is reshaping how capital moves, prioritizing real-time settlement over legacy batch processing.

Morgan Stanley highlights that stablecoins, when pegged to the dollar and integrated into programmable systems, offer immediate settlement capabilities. This contrasts sharply with traditional banking rails, which often involve multi-day delays. For enterprises, this means liquidity is no longer trapped in transit. The ability to settle transactions instantly reduces working capital requirements and minimizes counterparty risk, making native stablecoin infrastructure a practical tool for modernizing financial operations.

On the technology side, the adoption curve is steepening among enterprise payment platforms. According to McKinsey, companies like SAP and PayPal have begun offering native stablecoins to their business customers. This integration allows large corporations to settle invoices and manage cross-border payments within the same ecosystem they already use for ERP and commerce. By embedding these assets into existing platforms, these giants are lowering the barrier to entry for widespread tokenized cash adoption.

The result is a convergence of traditional finance and blockchain technology. As these systems mature, the distinction between "crypto" and "enterprise finance" continues to blur, replaced by a unified infrastructure designed for speed, transparency, and efficiency.

Tools for building on stablecoin rails

If you are building on stablecoin rails, the tooling landscape has shifted from experimental hacks to institutional-grade infrastructure. In 2026, you are no longer piecing together disparate APIs; you are choosing a stack that handles everything from issuance to compliance in one flow. Think of these tools as the plumbing for your financial app—hidden but essential. If the pipes leak, the whole system fails.

The most critical decision is picking your orchestrator. These platforms provide the core APIs for minting, burning, and transferring stablecoins across chains. Look for providers that offer native support for the major stablecoin standards (USDC, USDT, and emerging native tokens) and have robust SDKs for both web2 and web3 developers. Security is non-negotiable; your choice here dictates your risk profile.

For developers, the goal is speed and reliability. You want a tool that abstracts away the complexity of cross-chain bridges and gas management. This allows your team to focus on the user experience rather than debugging transaction failures. The right infrastructure lets you integrate stablecoin payments in days, not months.

To help you get started, we have curated a selection of technical guides and books that dive deeper into blockchain infrastructure. These resources cover the architectural patterns and security best practices you need to build a resilient stablecoin application.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!