Why native stablecoin infrastructure matters

The financial landscape is undergoing a structural shift. Stablecoins are moving beyond their origins as speculative DeFi primitives to become the backbone of global financial infrastructure. This transition is not merely about faster transactions; it is about replacing legacy settlement layers with programmable, real-time rails that institutions can trust.

Morgan Stanley highlights that by being pegged to the dollar and integrated into programmable infrastructures, stablecoins offer real-time settlement and low transaction costs that legacy banking systems struggle to match 1. This capability allows for instantaneous finality, a critical requirement for modern treasury management and cross-border payments.

Simultaneously, the monetization potential is expanding. As noted by Bessemer Venture Partners, new stablecoin-native equivalents can leverage wallets and cards to monetize like banks, earning interchange fees and a share of float interest 2. This economic model mirrors traditional banking but operates with greater efficiency and transparency.

The move toward native infrastructure means that stablecoins are no longer just a bridge asset but a foundational layer for finance. Institutions are building directly on these rails to reduce friction, lower costs, and enhance liquidity. This is the new standard for financial operations in 2026.

Core layers of the infrastructure stack

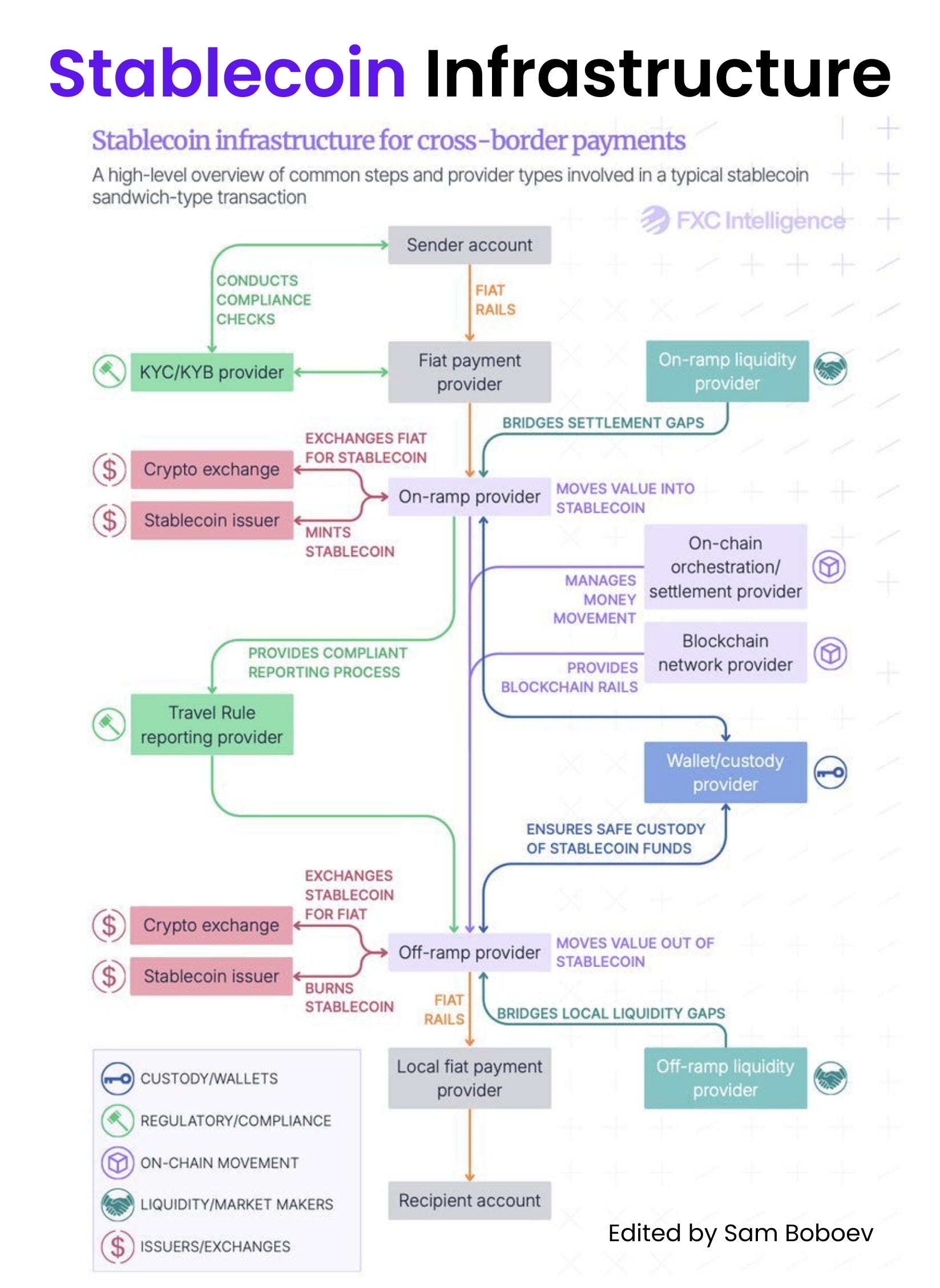

Building native stablecoin infrastructure requires more than just deploying a token on a blockchain. It demands a cohesive stack where technical protocols, financial reserves, and operational compliance work in concert. As Bridge outlines, this ecosystem rests on five interconnected pillars: the underlying blockchain, reserve management, digital custody, payment rails, and regulatory compliance.

Blockchain and Protocol Layer

The foundation is the distributed ledger itself. For native stablecoins, this means selecting a blockchain that offers finality, low latency, and sufficient throughput for high-volume transactions. Ethereum remains the dominant settlement layer due to its liquidity, though Layer 2 solutions and alternative chains are gaining traction for cost efficiency. The protocol must support smart contracts that govern minting, burning, and transfer logic without central points of failure.

Reserve Management and Transparency

A stablecoin’s value is only as credible as its backing. Native infrastructure requires real-time, verifiable reserve tracking. This involves holding assets in highly liquid, low-risk instruments like U.S. Treasury bills or cash equivalents. Regular attestation by independent third-party auditors is standard practice to ensure the circulating supply matches the reserve assets 1:1. This transparency is critical for maintaining user trust and regulatory standing.

Custody and Digital Wallets

Secure storage of both the stablecoin tokens and the underlying reserve assets is non-negotiable. Institutional-grade custody solutions use multi-signature wallets and hardware security modules (HSMs) to protect against theft and unauthorized access. For businesses, integrating these custody solutions via APIs allows for seamless settlement without taking direct custody of assets, reducing operational risk and liability.

Payment Rails and Interoperability

The infrastructure must facilitate fast, reliable transfers across different networks and fiat on-ramps. This includes integrating with payment processors and banking partners to bridge the gap between crypto and traditional finance. Interoperability protocols ensure that stablecoins can move freely between different blockchains and wallets, enabling global commerce without friction.

Compliance and Identity

Native stablecoin infrastructure is built with regulatory compliance at its core. This includes integrating Know Your Customer (KYC) and Anti-Money Laundering (AML) checks directly into the onboarding and transaction processes. Automated transaction monitoring systems flag suspicious activity in real-time, ensuring that the infrastructure adheres to the evolving legal frameworks in key jurisdictions.

How native stablecoin infrastructure enables institutional settlement

Traditional banking rails are built for a world that no longer exists. They rely on layered intermediaries, batch processing, and overnight settlement windows that tie up capital for days. Native stablecoin infrastructure changes this by moving settlement onto programmable blockchains. This shift allows for real-time finality and significantly lower transaction costs, which is essential for high-volume institutional operations.

As noted by Morgan Stanley, stablecoins integrated into programmable infrastructures offer real-time settlement and low transaction fees compared to legacy systems 1. This isn't just about speed; it's about capital efficiency. When funds settle instantly, institutions don't need to hold as much liquidity in reserve to cover potential delays or failures.

McKinsey highlights that stablecoins can be sent between two blockchain-based wallet addresses without opening an account at a traditional financial institution 2. This reduces friction and counterparty risk. For institutions, this means faster reconciliation and the ability to move capital globally with the same ease as sending an email.

Comparison: Traditional Rails vs. Native Infrastructure

The difference in operational mechanics is stark. The table below contrasts the core attributes of legacy banking systems with native stablecoin settlement.

| Feature | Traditional Banking Rails | Native Stablecoin Infrastructure |

|---|---|---|

| Settlement Time | T+1 to T+2 days | Real-time (seconds/minutes) |

| Transaction Cost | High (intermediary fees, FX spreads) | Low (network gas fees only) |

| Accessibility | Requires bank accounts and KYC | Direct wallet-to-wallet transfers |

| Capital Efficiency | Low (funds tied up in transit) | High (instant finality) |

This structural advantage allows institutions to scale operations without proportional increases in operational overhead. By removing the middlemen, native infrastructure turns settlement from a logistical bottleneck into a simple data transfer.

Compliance and reserve transparency

Institutional adoption of native stablecoin infrastructure hinges on one non-negotiable factor: trust. For finance professionals, trust is not a brand promise; it is a mathematical certainty derived from verifiable data. In 2026, the era of opaque reserve backing is over. Regulatory frameworks and market demands now require real-time, cryptographic proof that every unit of stablecoin in circulation is fully backed by high-quality liquid assets.

Transparency is no longer a competitive advantage; it is the baseline for participation in global financial markets. Native stablecoin infrastructure must integrate compliance directly into the protocol layer. This means embedding identity verification and transaction monitoring capabilities that satisfy anti-money laundering (AML) and know-your-customer (KYC) requirements without sacrificing the efficiency of blockchain settlement. Platforms like Chainlink have begun powering compliance-focused, transparent, and interoperable stablecoins that meet these rigorous demands, demonstrating how technical architecture can align with regulatory expectations Chainlink.

Reserve backing requires more than quarterly PDF reports. Institutional investors demand continuous, on-chain attestations. The infrastructure must support real-time reserve proofs, allowing auditors and regulators to verify asset composition instantly. This shift from periodic auditing to continuous verification reduces counterparty risk and ensures that stablecoins remain pegged even during periods of market stress. As the stablecoin issuance landscape matures, the distinction between compliant and non-compliant assets will widen, driving capital toward infrastructure that offers complete visibility DeFi Prime. Building this level of trust is essential for native stablecoins to function as a true settlement layer for global finance.

Market outlook and adoption signals

The market for native stablecoin infrastructure is shifting from experimental DeFi primitives to a core component of global financial rails. This transition is driven by institutional demand for programmable, settlement-ready assets that operate 24/7. The focus has moved beyond simple payments to complex financial operations, including treasury management, cross-border liquidity, and embedded finance.

Regulatory clarity remains the primary catalyst for this adoption. As jurisdictions like the EU with MiCA and the US with pending legislation define compliance standards, traditional financial institutions are more willing to integrate stablecoin infrastructure. This regulatory framework reduces counterparty risk and encourages banks to build native stablecoin solutions rather than relying on third-party wrappers.

Key players are evolving their service models to support this infrastructure. Issuers are offering more than just minting and redemption; they are providing compliance tooling, liquidity aggregation, and interoperability bridges. This comprehensive approach allows enterprises to deploy stablecoins without building the underlying technical stack from scratch.

Market indicators suggest a steady increase in transaction volume and total value locked (TVL) within stablecoin-specific ecosystems. This growth is not speculative but reflects real economic activity, such as payroll processing, supply chain finance, and international trade settlements. The infrastructure is becoming invisible yet indispensable, much like the SWIFT network it aims to complement or replace.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!