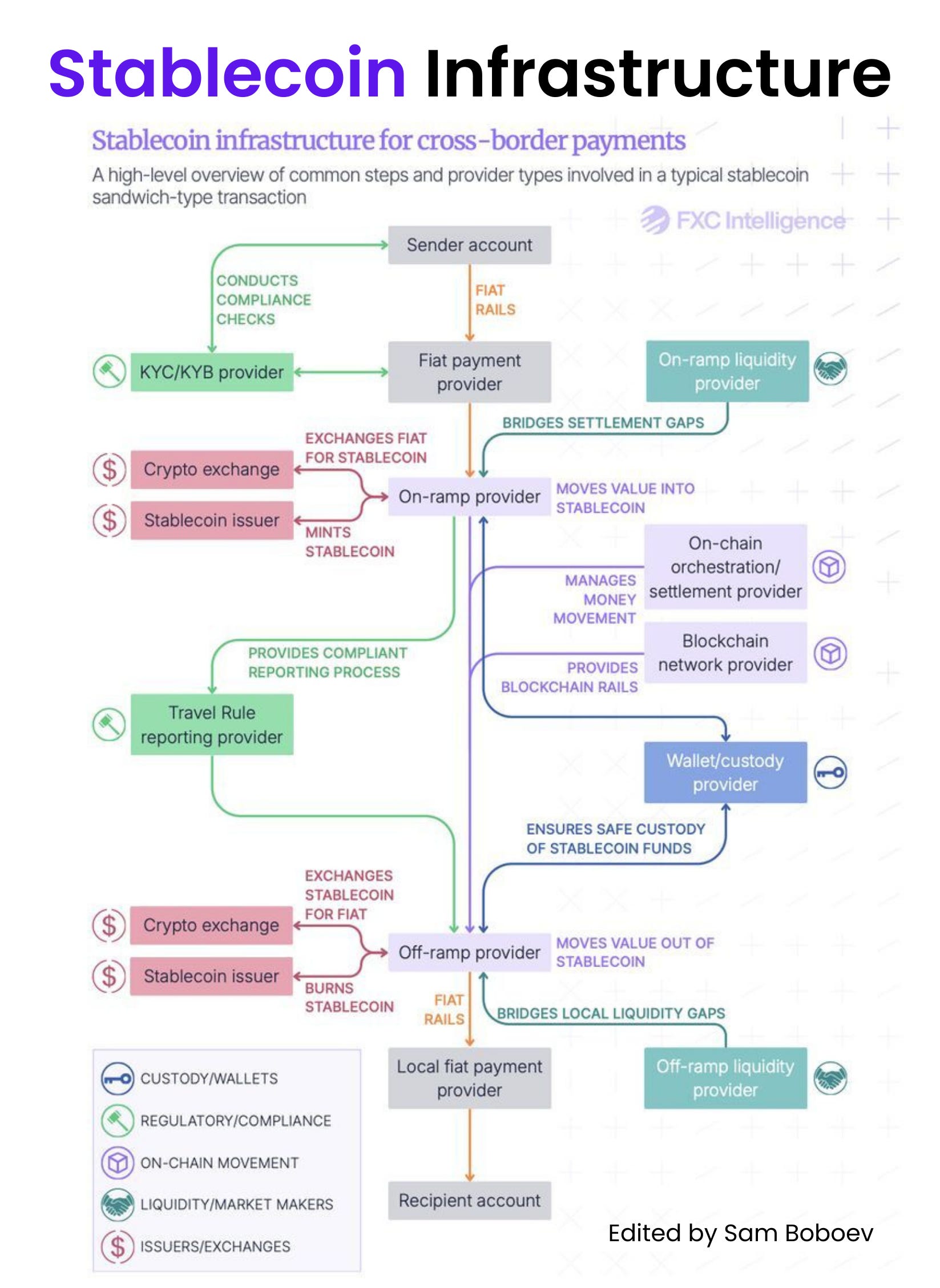

The shift to native stablecoin rails

The role of stablecoins is undergoing a fundamental structural change. They are moving beyond their origins as speculative DeFi primitives to become foundational elements of global financial infrastructure. This transition is driven by two converging forces: clearer regulatory frameworks and institutional demand for 24/7 settlement capabilities that traditional banking systems struggle to match.

Historically, stablecoins operated in the shadows of legacy finance, primarily serving crypto-native traders. Today, they are being integrated into mainstream payment rails. As McKinsey notes, stablecoins enable transfers between blockchain-based wallet addresses without requiring participants to open accounts at traditional financial institutions [McKinsey]. This disintermediation reduces friction and cost, allowing for near-instant settlement regardless of geographic location or banking hours.

Morgan Stanley highlights that by being pegged to the dollar and integrated into programmable infrastructures, stablecoins offer real-time settlement and low transaction fees [Morgan Stanley]. This efficiency is critical for modern commerce, where delays in settlement represent lost capital and operational risk. The ability to monetize these flows—through interchange fees and yield generation—positions stablecoin wallets as direct competitors to traditional banking products, as observed in recent analyses by BVP [BVP].

The Shift: Stablecoins are no longer just a crypto asset class; they are becoming the plumbing for real-time, global value transfer, bypassing traditional intermediary layers.

This evolution signals a long-term commitment to tokenized cash as a core component of future financial systems. For enterprises and developers, understanding this shift is essential to building infrastructure that meets the demands of a borderless, always-on economy.

The four layers of native stablecoin infrastructure

To understand how native stablecoins actually work, it helps to strip away the marketing and look at the technical stack. The system is built on four interconnected layers: the base network, the reserve and issuance mechanism, custody and wallets, and the payments or orchestration layer. Each layer handles a specific risk, and the "native" approach means these components are designed to communicate directly on-chain rather than through legacy banking rails.

Base network

This is the blockchain itself—Ethereum, Solana, or a dedicated L2. It provides the settlement finality and the public ledger where every transaction is recorded. For native infrastructure, the network must support high throughput and low fees to make micro-transactions viable. The choice of network dictates the gas costs and the speed at which funds can move, forming the foundation upon which all other layers are built.

Reserve and issuance

This layer manages the backing assets. When a user sends fiat currency, the issuer mints new tokens; when they burn tokens, the fiat is returned. In a native model, this minting and burning happens via smart contracts that verify the reserve balance in real time. This transparency ensures that the circulating supply is always fully backed, eliminating the opacity that plagued earlier, non-native stablecoin experiments.

Custody and wallets

Holding the keys is where security meets usability. Native infrastructure distinguishes between hot wallets for immediate transactional needs and cold storage for long-term reserve holdings. The infrastructure must provide secure key management that prevents unauthorized access while allowing seamless integration with decentralized applications. Without robust custody solutions, the risk of theft or loss undermines the entire system, regardless of how secure the underlying blockchain is.

Payments and orchestration

The final layer is the glue that connects the stablecoin to the real world. This includes APIs that allow merchants to accept payments, routing engines that find the best liquidity, and compliance tools that handle KYC/AML checks. Orchestration ensures that when a user clicks "pay," the transaction is routed efficiently across the network, settled instantly, and recorded for accounting purposes. This layer turns a digital token into a usable currency.

Custodial vs. non-custodial settlement models

When building native stablecoin infrastructure, the first architectural decision defines your entire operational risk profile: who holds the keys? The market has split into two dominant camps. On one side are custodial APIs like Circle and Stripe, which prioritize speed and regulatory ease. On the other are non-custodial middleware solutions, which prioritize key ownership and composability.

This choice isn't just technical; it's strategic. Custodial models let you launch faster by outsourcing compliance and custody to established financial rails. Non-custodial models require you to build or integrate the security layer yourself, but they grant you full control over the settlement logic. Understanding the tradeoffs is essential for selecting the right path for your specific use case.

Custodial APIs: Speed and Compliance

Custodial settlement providers act as the financial intermediaries. When you integrate a service like Stripe's crypto endpoints or Circle's Mint API, you are essentially renting their infrastructure. The provider holds the private keys, manages the KYC/AML checks, and handles the fiat on-ramps and off-ramps. This model significantly reduces your time to market because you don't need to build a compliance team or secure a banking charter.

However, this convenience comes with a loss of sovereignty. You are dependent on the provider's uptime, their regulatory standing, and their fee structure. If the provider changes its terms or faces regulatory scrutiny, your application is immediately exposed. This model is ideal for fintech apps that need to move quickly and want to minimize operational overhead.

Non-Custodial Middleware: Control and Flexibility

Non-custodial middleware shifts the burden of custody to the user or a decentralized key management service. In this architecture, the settlement layer is transparent and verifiable on-chain. You retain ownership of the keys, which means you also retain full control over the settlement logic. This is the preferred approach for DeFi protocols, DAOs, and platforms that require complex, programmable settlement flows.

The tradeoff is complexity. You must design robust key management systems, often using multi-signature wallets or threshold signature schemes to prevent single points of failure. You also bear the responsibility for ensuring your smart contracts and middleware comply with relevant regulations. While the initial build cost is higher, the long-term flexibility and lack of counterparty risk can be invaluable for scaling native infrastructure.

Side-by-Side Comparison

The following table compares the two approaches across key dimensions relevant to builders.

| Dimension | Custodial API | Non-Custodial Middleware |

|---|---|---|

| Key Ownership | Provider holds keys | User or app holds keys |

| Compliance Burden | Low (provider-managed) | High (self-managed) |

| Time to Market | Fast | Slower |

| Customization | Limited by API | Full control |

| Counterparty Risk | High | Low |

Choosing the Right Model

Your decision should align with your product's core value proposition. If your primary goal is to offer a seamless, regulated payment experience to a mass-market audience, a custodial API is the pragmatic choice. It allows you to focus on user experience rather than cryptographic security.

Conversely, if you are building a decentralized application, a DAO treasury, or a platform that requires programmable money flows, non-custodial middleware is the only viable path. It ensures that your settlement layer is as trustless and transparent as the rest of your stack. For many builders, a hybrid approach is emerging: using custodial rails for fiat on-ramps and non-custodial middleware for the actual stablecoin settlement.

Key Takeaways

- Custodial APIs offer speed and compliance at the cost of key ownership.

- Non-custodial middleware provides full control but requires significant security investment.

- The choice depends on whether your priority is rapid market entry or architectural sovereignty.

Market dynamics and issuer landscape

The stablecoin market has shifted from a DeFi niche to a core component of global financial infrastructure. As of early 2026, the landscape is dominated by a clear hierarchy of issuers, with USDT (Tether) and USDC (Circle) maintaining the vast majority of market share. This concentration is not accidental; it reflects the deep liquidity and institutional trust these native stablecoins have built over years of integration into trading pairs, payment rails, and enterprise settlement layers.

Tether continues to lead in total circulating supply, largely driven by its dominance in high-volume, cross-border trading environments and emerging markets where speed and low fees are paramount. However, Circle’s USDC has carved out a distinct advantage in regulated, US-domiciled infrastructure. For enterprises and financial institutions building compliant settlement layers, USDC’s transparency, regular attestation reports, and alignment with US regulatory frameworks make it the preferred choice for native stablecoin integration. This trend underscores a broader industry move toward standardized, auditable infrastructure rather than purely speculative yield generation.

The emergence of new issuers like PayPal’s PYUSD highlights the growing interest from traditional fintech players in launching regulated, US-based stablecoins. While still smaller in scale compared to Tether and Circle, PYUSD represents a significant signal: major financial brands are entering the space with a focus on compliance and integration with existing payment networks. This competition is likely to drive further innovation in native stablecoin infrastructure, particularly in areas like programmable money, real-time settlement, and cross-chain interoperability.

| Issuer | Market Position | Primary Use Case |

|---|---|---|

| Tether (USDT) | Largest by supply | Cross-border trading & emerging markets |

| Circle (USDC) | Second largest, high compliance | Enterprise settlement & regulated DeFi |

| PayPal (PYUSD) | Emerging, fintech-backed | Retail payments & PayPal ecosystem |

The competitive dynamic between these issuers is shaping the technical requirements for native stablecoin infrastructure. Enterprises must now evaluate not just the technical robustness of a stablecoin’s underlying chain, but also the issuer’s regulatory posture, liquidity depth, and integration capabilities. This shift from a purely technical evaluation to a holistic infrastructure assessment is critical for building resilient, future-proof payment systems.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!