What makes a native stablecoin strategy work

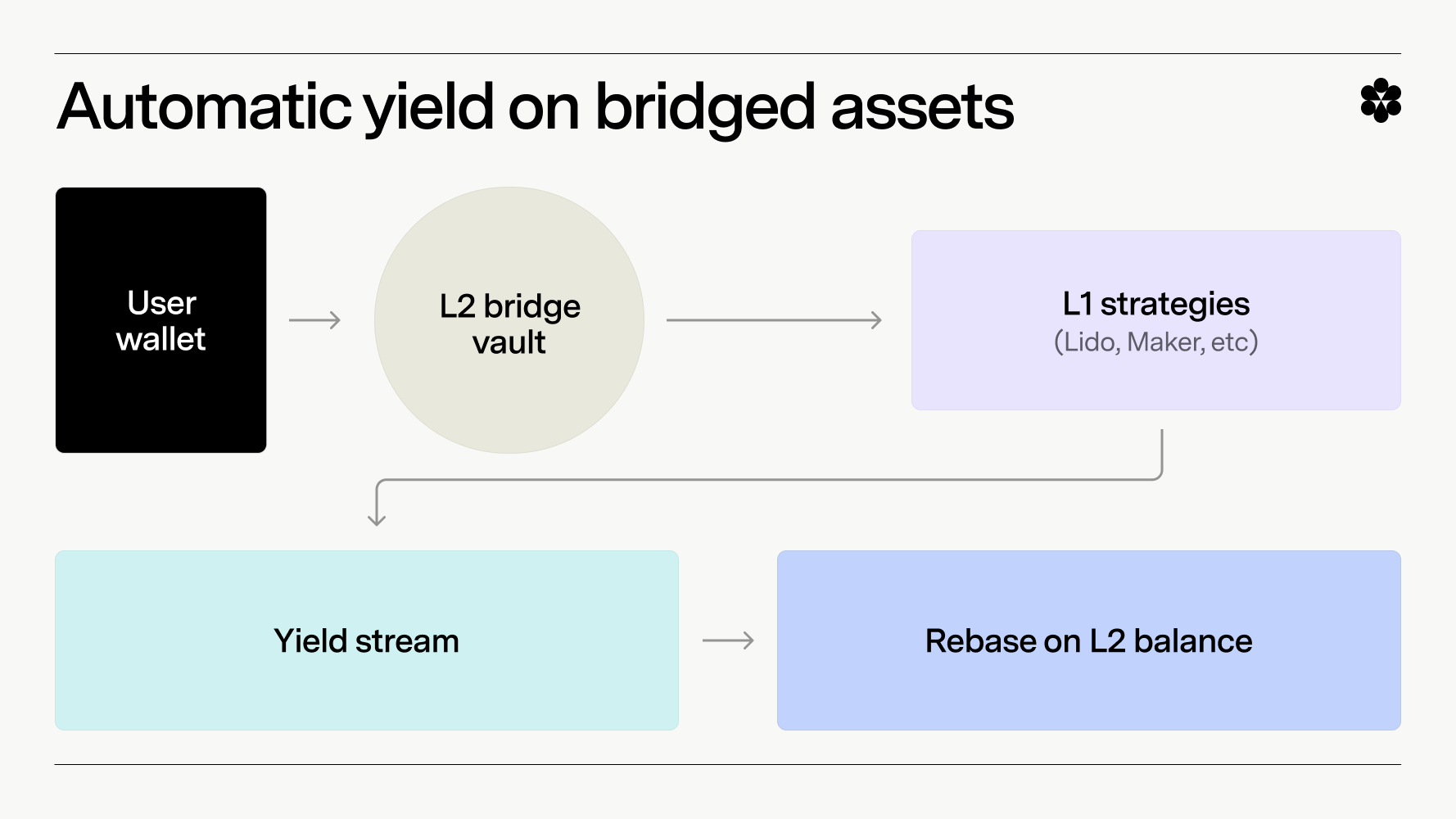

A native stablecoin strategy relies on assets that are minted, traded, and settled directly on their home blockchain. This is distinct from bridged or wrapped tokens, which represent an asset on a foreign chain via a third-party bridge. The difference matters because it eliminates the counterparty risk and latency associated with cross-chain transfers, creating a cleaner environment for real-time settlement infrastructure.

When a stablecoin is native to a chain, its liquidity and settlement logic are baked into the base layer or its primary Layer 2. For example, a Bitcoin-native stablecoin uses BTC locked in a vault on Bitcoin itself as collateral, never requiring the underlying asset to leave the Bitcoin network. This contrasts with wrapped versions that rely on custodial bridges, introducing a single point of failure and additional confirmation delays.

This distinction is critical for high-frequency financial operations. By keeping the asset and its settlement layer in the same ecosystem, institutions can achieve near-instant finality without the reconciliation overhead of bridged assets. The IMF has noted that stablecoins can significantly improve global payment efficiency when they operate within a streamlined, native framework rather than a fragmented, bridge-dependent one.

The strategic advantage lies in the reduction of operational friction. Native stablecoins allow for direct on-chain collateralization and settlement, which is essential for building robust real-time payment rails. While bridged assets offer cross-chain flexibility, they introduce complexity that can undermine the very speed and security a native strategy aims to provide.

Choosing the right settlement use case

Not every payment needs to move on-chain. The most effective native stablecoin strategies target high-friction flows where traditional rails are too slow, too expensive, or simply unavailable. By focusing on specific business applications, you can justify the infrastructure shift and demonstrate clear ROI before scaling.

B2B cross-border payments

International trade often involves multiple intermediaries, each taking a cut and adding days to the settlement window. Native stablecoins allow businesses to send payments directly between wallet addresses, bypassing the correspondent banking network. According to McKinsey, this infrastructure enables payments without requiring both parties to hold traditional bank accounts, reducing friction for emerging market partners. The result is near-instant settlement and significantly lower transaction costs.

Payroll for global teams

Paying remote workers across borders introduces currency conversion fees and delayed access to funds. Native stablecoins solve this by allowing employees to receive stable assets directly into their digital wallets. This is particularly impactful for teams in regions with volatile local currencies or limited banking access, such as parts of Latin America, Africa, and Southeast Asia. Workers can hold, spend, or convert their earnings instantly without relying on expensive remittance services.

Real-time treasury management

Traditional treasury operations often involve idle cash sitting in transit between accounts. Native stablecoin infrastructure enables real-time visibility and movement of funds. Companies can automate payouts, rebalance liquidity across jurisdictions, and execute payments during off-hours without waiting for banking hours. This operational agility turns treasury management from a reactive administrative task into a strategic, real-time function.

Settlement comparison

The following table highlights the operational differences between traditional SWIFT transfers and native stablecoin settlement for high-volume business flows.

Building compliant settlement infrastructure

Launching a native stablecoin strategy requires more than just code; it demands a settlement layer that satisfies both technical efficiency and regulatory scrutiny. A native stablecoin—specifically one issued on Bitcoin Layer 1 using native BTC as collateral—offers a unique advantage: it never requires assets to leave the Bitcoin network. This eliminates bridge risk, but it introduces complex custody and liquidity challenges that traditional finance (TradFi) infrastructure must solve.

Custody and Compliance

For financial institutions, custody is the primary compliance hurdle. You cannot use consumer-grade wallets. Instead, you need institutional-grade custody solutions that provide multi-signature security, audit trails, and integration with existing treasury management systems. Fireblocks and similar providers offer the infrastructure needed to manage these assets securely while maintaining the transparency required by regulators. The goal is to treat the stablecoin not as a speculative asset, but as a settlement instrument with strict governance.

Liquidity and Reserve Management

Liquidity in a native stablecoin system is tied directly to the collateralization ratio of the underlying BTC. Because the collateral never leaves Bitcoin, you must ensure that your settlement infrastructure can handle real-time price fluctuations without triggering liquidations that disrupt payments. This requires robust oracle integration to track BTC prices accurately and automated mechanisms to maintain the peg. Unlike fiat-backed stablecoins that rely on bank deposits, native stablecoins rely on on-chain liquidity pools and decentralized finance (DeFi) protocols that must be rigorously audited.

Regulatory Alignment

Regulatory adherence is not optional. You must align with emerging frameworks such as the EU’s MiCA or US state-level money transmitter laws. This means implementing KYC/AML checks at the wallet level and ensuring that your stablecoin issuance is transparent and auditable. Official sources, including central bank reports and regulatory filings, should be your primary reference for compliance standards. Ignoring these requirements can lead to severe penalties and loss of trust.

Technical Integration

Finally, your settlement infrastructure must be able to interact seamlessly with existing payment rails. This means building APIs that allow traditional payment processors to initiate and settle transactions in native stablecoins. The technology should abstract away the complexity of blockchain interactions for end-users, providing a familiar experience while leveraging the speed and finality of the underlying blockchain.

Market research for stablecoin adoption

Before building infrastructure, you need to validate that a real demand exists. Stablecoins are not a one-size-fits-all solution; they serve distinct purposes depending on the user’s financial context. Your research should map these use cases to specific demographics, starting with the unbanked and underbanked populations in emerging markets.

In regions with high inflation or limited access to traditional banking, stablecoins offer a lifeline. Research should quantify the volume of cross-border remittances and local transaction needs that current banking rails fail to meet efficiently. For instance, users in Latin America or Southeast Asia often rely on stablecoins to preserve value against local currency volatility. Understanding the pain points of these groups—such as high fees or slow settlement times—helps define the value proposition of a native stablecoin strategy.

For developed markets, the target demographic shifts toward crypto-native users and businesses seeking operational efficiency. Here, the focus is on speed, cost, and programmability. Market research should analyze how existing stablecoins like USDT or USDC are currently used in DeFi protocols, gaming economies, and merchant payments. Identify where friction exists: perhaps it is the gas fees on Ethereum that drive users to alternative chains, or the lack of native settlement layers that slows down real-time commerce.

The competitive landscape is equally critical. You must assess who else is offering similar solutions and where their gaps lie. Look at the strategies of established players like Circle (USDC) and Tether (USDT), as well as newer entrants like PayPal’s PYUSD. Pay attention to their regulatory compliance strategies, reserve transparency, and integration partnerships. A native stablecoin often competes on the basis of being embedded directly into a blockchain’s native ecosystem, offering lower costs and faster finality than bridged assets. Understanding these competitive advantages will help you position your infrastructure not just as another token, but as a necessary layer of financial utility.

Common questions about native stablecoins

Understanding the mechanics of native stablecoins requires separating the asset class from the infrastructure. Unlike wrapped assets that bridge value across chains, a native stablecoin is minted and redeemed directly on its host blockchain, using the chain’s native currency as collateral without moving it off-network. This eliminates bridge risk and simplifies settlement.

Stablecoin strategy focuses on using these low-volatility assets for real-time payments and treasury management. By pegging to fiat or commodities, they provide the stability needed for commercial transactions while leveraging blockchain efficiency. The goal is to create a reliable medium of exchange that avoids the wild swings of speculative crypto.

The distinction between native and non-native crypto lies in their origin. Native tokens are created directly on the base layer to secure the network, whereas non-native tokens are issued on platforms built atop that chain. For a native stablecoin, the stability mechanism is intrinsic to the primary blockchain, ensuring that the asset remains anchored to the underlying network's security.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!