Map your settlement requirements

Before selecting a blockchain or stablecoin issuer, define the specific business use case. The settlement layer must match the transaction volume, finality needs, and regulatory tier of your operation. A B2B payment rail requires different throughput and compliance features than a B2C consumer wallet or a cross-border remittance service.

The global fiat-backed stablecoin supply exceeded $273B in March 2026, signaling a shift from DeFi primitive to global financial infrastructure (BVP/Visa). This scale demands infrastructure that can handle high-frequency settlements without clogging the network.

B2B Payment Rails

Business-to-business transactions typically involve larger ticket sizes and lower frequency. Here, finality matters more than speed. You need a settlement layer that offers irrevocable confirmation within seconds, reducing counterparty risk. Compliance is equally critical; your infrastructure must integrate with existing ERP systems and support KYC/AML checks at the enterprise level.

B2C Consumer Wallets

Consumer-facing applications prioritize low fees and instant availability. Users expect micro-transactions to clear immediately, often on mobile devices. The settlement layer must support high throughput to handle peak loads without latency spikes. Regulatory compliance here focuses on consumer protection and data privacy, requiring robust identity verification flows that do not frustrate the user experience.

Cross-Border Remittance

Cross-border payments require interoperability between different financial systems and jurisdictions. The settlement infrastructure must bridge legacy banking rails with blockchain networks, ensuring that funds move across borders without getting stuck in correspondent banking delays. Regulatory arbitrage is a risk; you must navigate varying AML regulations in each transit country.

Regulatory Tier Alignment

Your settlement requirements must align with the regulatory tier of the stablecoin issuer. Tier-1 issuers (e.g., Circle, Paxos) offer full reserve backing and regular attestations, suitable for institutional funds. Tier-2 or decentralized stablecoins may offer lower fees but higher volatility risk. Choose the tier that matches your risk appetite and legal obligations.

Select the underlying blockchain layer

Choosing the right blockchain for your stablecoin infrastructure comes down to three hard metrics: transaction cost, finality speed, and institutional custody support. You aren't just picking a network; you're picking the rails your money moves on. If the rails are too expensive or too slow, your product fails before it launches. If the custody options are weak, institutional partners walk away.

Start by comparing the leading candidates side-by-side. Ethereum L2s like Base and Arbitrum offer low fees and deep liquidity, while dedicated "stablechains" like Stripe's EVM-compatible network offer built-in compliance hooks. Solana provides high throughput but requires different technical architecture. Use the table below to weigh the trade-offs for your specific use case.

| Network | Avg. Tx Cost | Finality | Institutional Custody |

|---|---|---|---|

| Ethereum L2 (Base/Arb) | <$0.01 | ~2 sec | Strong (Fireblocks, Copper) |

| Solana | <$0.001 | ~400 ms | Growing (Fireblocks, Anchorage) |

| Stripe EVM Stablechain | Low | ~2 sec | Native (Stripe integration) |

| Ethereum L1 | $1-$20+ | ~12 sec | Strong (Legacy standard) |

Morgan Stanley notes that stablecoins offer real-time settlement and low transaction costs when integrated into programmable infrastructures, but the choice of layer dictates your scalability ceiling [src-serp-2]. If you are targeting high-frequency B2B payments, the $0.01 difference between an L2 and an L1 becomes significant over millions of transactions. If you are targeting enterprise compliance, the native integration of Stripe's stablechain might outweigh the lower fees of Solana. Don't overengineer the initial layer. Pick the network that aligns with your primary user base. If your users are already on Ethereum, stick to an L2. If you are building a new payment rail from scratch, evaluate the dedicated stablechains emerging in 2026. The goal is to minimize friction, not maximize technical complexity.

Integrate compliance and oracle layers

Institutional adoption requires more than just a token; demands a middleware layer that guarantees transparency and regulatory adherence in real time. You need to connect on-chain reserve verification with off-chain identity checks to meet the scrutiny of global financial markets. This integration ensures that every transaction is backed by auditable assets and compliant participants.

Connect real-time reserve verification

Stablecoins must prove their backing continuously, not just during quarterly audits. Use oracle networks like Chainlink to pull data from traditional banking APIs and custodial wallets directly onto the blockchain. This creates a transparent, tamper-proof record of reserves that institutions can verify instantly. Without this live feed, the token remains a black box, which is unacceptable for enterprise treasury management.

Implement identity and compliance checkpoints

Regulatory requirements like AML (Anti-Money Laundering) and KYC (Know Your Customer) must be embedded into the transaction flow. Integrate compliance oracles that check wallet addresses against sanctions lists and verify user identities before allowing transfers. This middleware acts as a gatekeeper, ensuring that only verified entities can interact with the stablecoin. It transforms the token from a permissionless asset into a compliant financial instrument suitable for institutional use.

Enable cross-chain interoperability

To function as true infrastructure, the stablecoin must move fluidly across different blockchain networks. Implement cross-chain messaging protocols that allow the token to be locked on one chain and minted on another, maintaining its peg and integrity. This interoperability ensures that liquidity isn't trapped in isolated silos. It allows the stablecoin to serve as a universal settlement layer, connecting diverse financial ecosystems without friction.

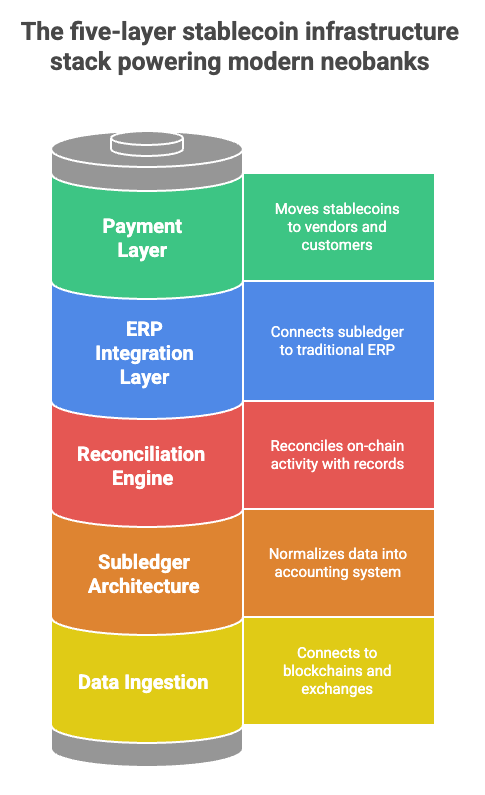

Connect to enterprise payment rails

Bridging on-chain stablecoin infrastructure with off-chain banking and ERP systems is where the technology moves from speculative asset to operational utility. For finance professionals, this means integrating digital dollars into legacy workflows without forcing staff to abandon familiar tools like SAP, Oracle, or Stripe.

The goal is to make stablecoin payments feel identical to traditional wire transfers or ACH payments from the perspective of the accounts payable and receivable teams. When done correctly, the blockchain becomes an invisible settlement layer rather than a new interface to learn.

Map stablecoins to existing ERP workflows

Most enterprise resource planning systems do not natively support blockchain wallets. Instead, you connect stablecoin rails through existing payment gateways or specialized middleware that translates on-chain transactions into standard accounting entries. Platforms like SAP now offer native stablecoin capabilities for business customers, allowing invoices to be settled in USDC or other pegged assets while maintaining standard ledger formats.

Route transactions through established payment processors

Rather than building direct blockchain connections, leverage established payment processors that have already integrated stablecoin support. Stripe, for example, provides infrastructure that allows businesses to accept and settle stablecoin payments while managing the underlying crypto custody and compliance requirements. This approach reduces technical debt and ensures that transaction data flows directly into your existing financial reporting tools.

Automate reconciliation with on-chain data

The primary advantage of this integration is real-time reconciliation. Unlike traditional bank transfers that can take days to clear, stablecoin transactions settle in minutes. By connecting your ERP system to the blockchain network, you can automate the matching of payments to invoices as soon as the transaction is confirmed on-chain, significantly reducing the time your finance team spends on manual reconciliation.

As an Amazon Associate, we may earn from qualifying purchases.

Verify compliance and audit trails

Before fully integrating stablecoin rails, ensure your connection points meet regulatory requirements. Enterprise payment processors typically handle the heavy lifting regarding KYC/AML compliance, but you must verify that the transaction data they return is sufficient for your internal audit needs. The blockchain provides an immutable record, but your ERP system must be configured to capture and store this data in a way that satisfies financial auditors.

Monitor market metrics and liquidity

Once your infrastructure is live, the work shifts to maintenance. You need to watch three specific signals: market share, liquidity depth, and peg stability. Ignoring these metrics allows your stablecoin to become a ghost town, even if the underlying code is perfect.

Start with market share. The global fiat-backed stablecoin supply exceeded $273 billion in March 2026, growing 40x from $6.8 billion in March 2020 1. This rapid expansion means competition is fierce. You must track your total value locked (TVL) and transaction volume against major competitors like USDC and USDT. If your growth stalls, it usually indicates a liquidity or trust issue, not a technical one.

Next, monitor peg stability. A stablecoin that drifts more than a few basis points from $1.00 loses its utility as a medium of exchange. Use a TradingView chart to track the spread between your token and the USD in real-time. Sudden deviations often signal a liquidity crunch or a regulatory scare. If the peg breaks, you need a predefined response plan, such as activating a redemption mechanism or injecting reserve assets.

Finally, assess liquidity depth. Shallow order books lead to high slippage, which scares away institutional users. Check the depth of your liquidity pools on decentralized exchanges and the availability of your tokens on centralized exchanges. Consistent volume is more important than occasional spikes. If liquidity dries up, your infrastructure becomes too expensive to use for even small transactions.

Verify your deployment checklist

Before going live, run through a final verification sequence. This step ensures that every technical, compliance, and liquidity component is active and communicating correctly. Think of this as the pre-flight inspection for your stablecoin infrastructure; a single missed connection can halt transactions or trigger compliance flags.

Start by confirming that your on-chain reserve attestations are current and visible to all relevant nodes. Next, validate that your payment gateway APIs are routing transactions through the correct stablecoin pairs without latency spikes. Finally, test the end-to-end flow with a small, real-money transaction to ensure settlement matches your ledger expectations.

Stripe notes that stablecoin infrastructure relies on systems that maintain steady value and reliable transfers during peak loads.

-

Reserve attestations updated and visible

-

Payment gateway APIs routing correctly

-

End-to-end test transaction settled

-

Compliance filters active for jurisdiction

-

Liquidity pools funded and rebalanced

Frequently asked: what to check next

Building native stablecoin infrastructure requires navigating complex regulatory and technical landscapes. These questions address the most common hurdles developers and finance professionals face when launching compliant, scalable systems.

Work through Native Stablecoin Infrastructure

No comments yet. Be the first to share your thoughts!